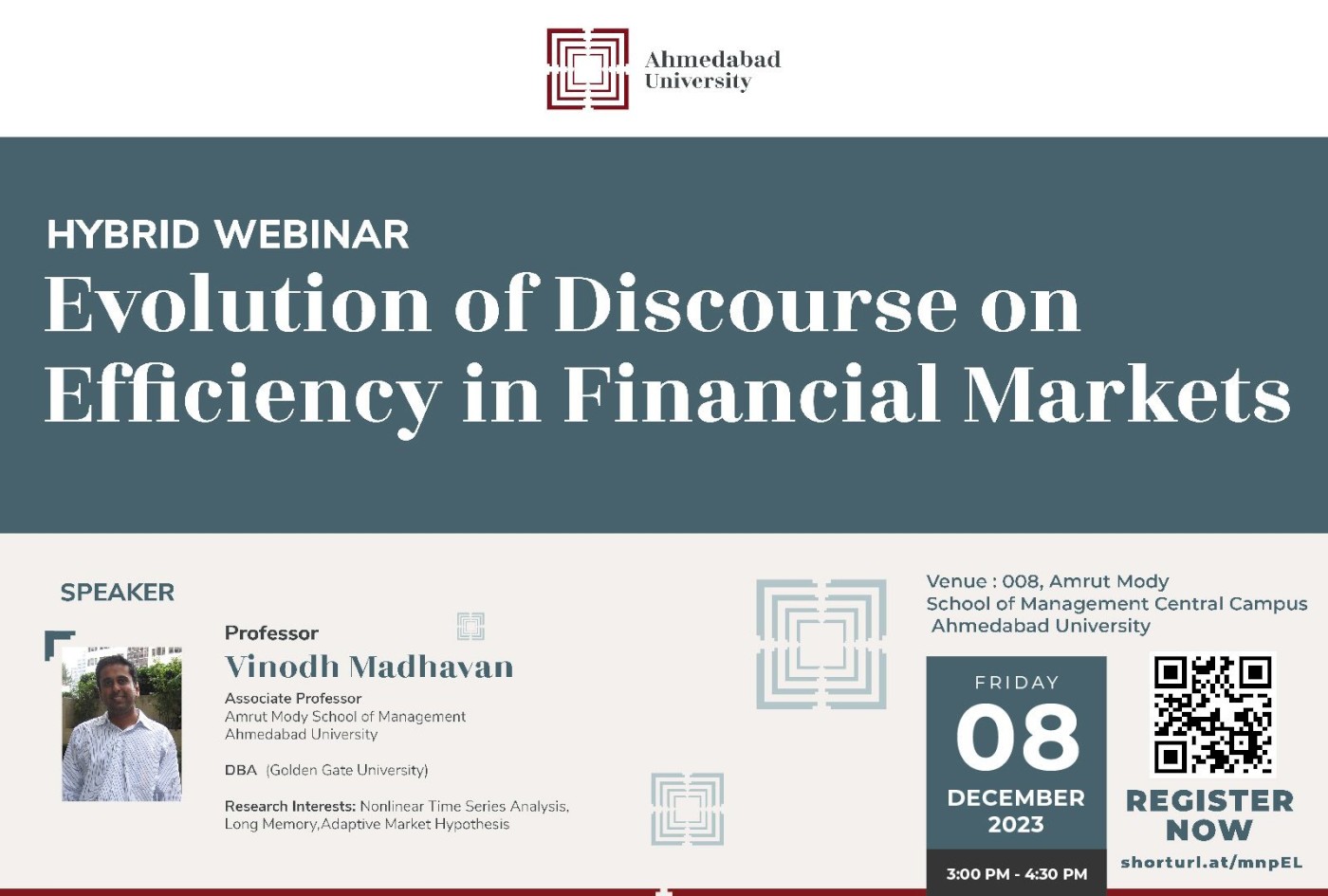

Evolution of Discourse on Efficiency in Financial Markets

A major intellectual advancement in the field of Finance is the Efficient Market Hypothesis (EMH). Market efficiency could be broadly classified into three forms namely, weak-form, semi-strong form, and strong-form efficiency. Weak form of market efficiency would imply that the past history of price movements pertaining to any asset is already impounded in the current price of the asset. Should a market be found to be semi-strong efficient, then asset prices should reflect all publicly available information. The strong-form of market efficiency would imply that asset prices should not just reflect all publicly available information in the marketplace, but also privately held information. Prevalence of strong-form of efficiency would preclude the possibility of making profits by insider trading activities. Over time, a substantial body of literature challenging EMH developed and this brought to light the limitations of econometric tests employed to ascertain market efficiency. Having said so, there appeared to be no room for compromise between proponents and opponents of EMH as late as 2004. It is at this juncture that Adaptive Market Hypothesis (AMH) offered an intellectual edifice that facilitated coexistence of opposing perspectives on EMH. Grounded in evolutionary biology, AMH offers an intellectual framework that helps researchers overcome the fallacy of treating market efficiency as an all or nothing static phenomenon. Till date, AMH continues to play a defining role when it comes to examining behaviour of financial markets using methodologies that possess different theoretical antecedents. The canvas of EMH is no longer monochromatic but rather more variegated in nature. This webinar will offer an overview of the evolution of discourse on market efficiency in the context of financial markets.